Rent vs Buy: Comparing the Costs of Owning vs. Renting a Home

Senior Manager of Sales at Truehold - A Thought-Leader in Real Estate

Homeownership comes with a lot of perks: there are potential tax benefits, a sense of permanence, and the satisfaction of knowing that your home truly belongs to you. But owning a home can also be expensive and tiresome. Freedom from key costs can make renting a much more appealing option.

Compared to homeownership, rental costs are more straightforward. There are some costs, however, that potential renters tend to overlook. For example, your rent can change when the term of your lease ends, forcing you to decide between moving or paying higher rent. So, which is the better option? What is the cost of owning a home vs. renting?

If you’re trying to decide whether to rent vs buy a home, it's important to understand the different expenses associated with each option so you can make an informed decision. It’s also a good idea to look into alternative options that may simplify this process for you. If you’ve been wondering, “Should I rent or sell my home?”, then a sell and stay transaction may be the best option for you. This offers an innovative home equity solution for a homeowner who wants to minimize some of the financial or physical burdens of homeownership without moving.

Homeownership Costs

Owning a home comes with various annual and monthly housing costs. While not applicable to everyone, the majority of homeowners are familiar with these expenses beyond just the home price:

Home Loans and Closing Costs

Your monthly mortgage payment isn’t always the only monthly expense. When you buy a home, you’re also taking on costs that relate to the real estate transaction itself. There are sales commissions, document fees, service fees, and other expenses that you’ll have to account for. If you have a loan with a fixed interest rate, on the other hand, your mortgage rate will be steady each month.

Some people opt for adjustable rate mortgages (ARMs) that can go up or down depending on the current mortgage interest rate. While this allows you to take advantage of falling rates, it can make budgeting difficult.

Depending on where you live, property tax can be a significant expense. The amount you pay in property tax is based on your home's value. When your land and structure are reassessed, if the value of your property increases, your property tax rate generally does as well. This can make it difficult for older homeowners living in areas where home values are increasing drastically. If you’re looking for ways to lower your property tax, check out tips to lower property tax.

Unlock your property's potential with Truehold's sale-leaseback

Click hereInsurance

Insurance on your home isn’t just prudent, it's almost always required by the mortgage lender. Even after you own your home, it’s important to keep your home insured to avoid losing your investment in a fire or natural disaster.

The monthly cost of homeowners insurance is usually fairly substantial. High deductible plans may keep your monthly payments lower, but then leave you with less coverage when you need it. Some areas require flood insurance, and this can be a major added expense.

Maintenance

Every home will require repairs and maintenance at some point. If you own your home, you’re probably familiar with routine maintenance like landscaping, checking for leaks, testing your smoke detectors, removing snow, etc. But in addition to these routine chores, remember that just about everything in your home has a lifespan, and someday, you’ll need to pay for a repair or replacement.

Roofs, for instance, usually last 20 to 30 years. You’ll need to have your roof repaired and eventually replaced to prevent damage to the structure underneath.

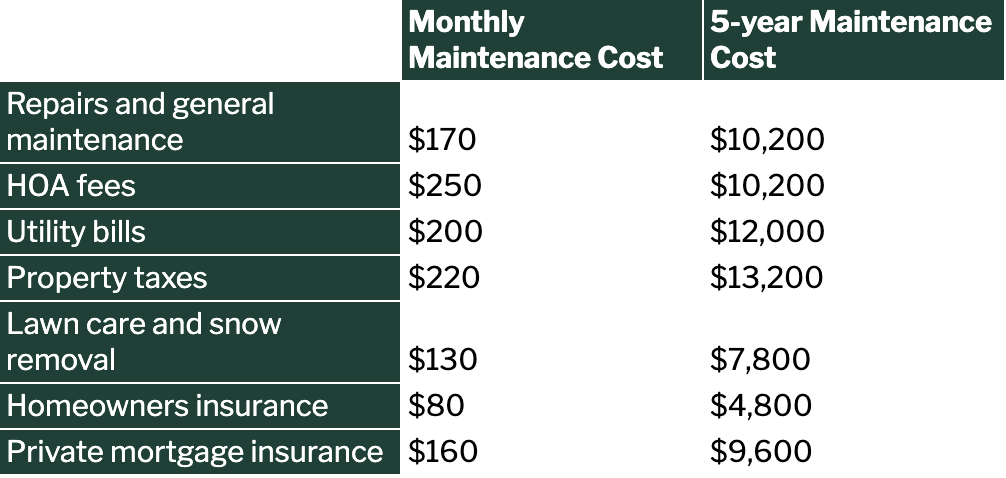

Other structural repairs include: leaky plumbing, damage to floors, broken or drafty windows and doors, HVAC equipment, gutters, and garage doors. And don’t forget all the appliances you own: the dishwasher, your washer and dryer, stoves, refrigerators, and more. Here’s how the average household maintenance costs could add up over time:

While most homeowners expect occasional repairs and replacements, it is difficult to predict exactly when and how to budget for these. The most frustrating situation is when multiple repairs are needed at once, and the homeowner is stuck with a huge bill.

Homeowners Association (HOA) Fees

If you live in a homeowners association (HOA) community, then you’ll have monthly payments or quarterly fees which may cover certain utilities and services like trash collection or snow plowing. They can also grant you access to amenities like a community pool or tennis courts.

Another expense some people don’t expect is special assessments. In some HOA communities, there are large and expensive repairs that must be made to a common area or shared building. Homeowners in the community share in the expense, but it can still run into the tens of thousands of dollars for each home.

Rental Costs

Rent

One major difference between renting vs buying a home is the stability of the expenses. For the term of your lease, you’ll pay the same rent each month. Some communities offer a lower rent payment for a longer lease term, but shorter leases will be at an increased cost.

Renting usually carries with it the added expense of having to pay the first and last month’s rent upfront along with a security deposit. At the end of the lease, the landlord inspects your rental property, and if there is more than normal wear and tear, you pay for it out of your deposit.

When your lease term is up, your monthly rent can change, and this can certainly be challenging financially - especially if the increase is large.

Maintenance and Utilities

As a renter, the maintenance costs are paid for by your landlord. This means you don’t need to worry about covering large and unpredictable expenses for broken appliances. If the landlord believes you may have caused the damage, you can be on the hook for the repairs.

You may pay for some or all of your utilities when you rent. This is one expense that is shared between owning a home and renting, since everyone needs to pay for the electricity, gas and water they use, along with trash and sewer fees.

Truehold’s Sell and Stay Transaction

Truehold ’s sell and stay transaction is a great option for homeowners who want to gain freedom from some key homeownership costs without downsizing or moving to a new rental property. Considerations when downsizing are important, but with Truehold, you sell your home and then you continue to live in your home as a renter. Truehold covers essential repairs, property tax, and property insurance.

As you can see, there are a variety of advantages of renting a home — especially if its a home you’ve already grown to love! If you think Truehold might be the right option for you, give us a call at 314-353-9757!

Senior Manager of Sales at Truehold - A Thought-Leader in Real Estate

Lucas Grohn is a Senior Manager of Sales at Truehold, leading a team of local market experts and overseeing the brand’s sales outreach strategy. Lucas has been a thought-leader in the real estate industry for more than a decade. He got his start working alongside institutional investors and has since found himself in a myriad of different roles.From being a Managing Broker, to training new agents at some of the country's most well known real estate brands (Redfin, Zillow, RE/MAX). He spends his free time hanging with his family on the beach in Georgia and taking pictures of two daughters (1&4).